Maintaining healthy cash flow is paramount to sustaining operations, fueling growth, and seizing new opportunities.

However, fluctuating revenue streams, unexpected expenses, and seasonal variations often challenge the cash reserves.

In such scenarios, seeking the right financing solution can be a game-changer for small businesses looking to bridge financial gaps and keep their operations running smoothly.

Read on to find 4 best cash flow loans for small businesses to unlock financial stability.

Let’s dive in!

What is a Cash Flow Loan?

A cash flow loan is a business loan issued based on your expected cash flow rather than traditional collateral or assets.

Thus, the lender evaluates your ability to generate sufficient cash flow from your business operations to repay the loan amount and interest within a specified period.

You can use cash flow loans for various business purposes, such as:

💰 Working capital needs,

💰 Financing growth opportunities,

💰 Purchasing inventory,

💰 Expanding operations or

💰 Covering operational expenses.

A Cash Flow Loan vs. Asset-Based Loan: What’s The Difference?

Cash flow loans and asset-based loans are 2 different types of financing that differ by the method lenders use to evaluate repayment options.

.webp)

In terms of risk management, it may be better to apply for a cash flow loan since you don’t compromise the company’s property.

5 Steps of Cash Flow Lending

Although there are certain nuances and differences between lenders, but below is how cash flow loans typically work:

✨ Application Process

During the application process, you provide information about your financial history, revenue, expenses, and cash flow projections.

Then, lenders evaluate the business's financial health, creditworthiness, and ability to generate sufficient cash flow to repay the loan.

✨ Loan Approval

If the lender approves the loan, they determine the loan amount, interest rate, repayment terms, and other conditions based on your business's cash flow situation.

As we’ve already mentioned, collateral isn’t the key factor since the focus is more on the business's ability to repay the loan from its cash flow.

✨ Funding

Once you agree upon the loan terms, the lender transfers the funds to your business. Thus, you can use the loan to buy equipment, expand your business, etc.

✨ Repayment

The lender requires regular monthly or quarterly payments to repay the loan, including both principal and interest.

The repayment schedule is based on your business's cash flow cycles to ensure manageable payments.

✨ Monitoring and Compliance

Lenders usually monitor your business's financial performance to ensure the cash flow remains sufficient to repay the loan.

Naturally, you must comply with the loan terms and provide updated financial information that your lender requests.

4 Best Cash Flow Loans for Small Business

Business cash flow loans come in many forms, but we’ve handpicked 4 solutions that may suit your small business best.

1. Lines of Credit

Business lines of credit are among the most popular cash flow loans due to their flexibility.

You can choose to borrow any amount up to the credit limit at any time, with the interest charged on the amount of money you’ve actually borrowed, not the entire credit limit.

This makes it more cost effective than traditional loans.

It is a revolving type of loan, meaning the credit line replenishes as you repay it.

As a result, you have ongoing access to funds without needing to reapply for a new loan each time.

Lines of Credit: Key Pros and Drawbacks

🟢 Great flexibility.

🟢 Higher credit limits.

🟢 Good to cover short-term expenses or unexpected costs.

🔴 May cause you to overborrow and accumulate more debt than you can pay.

🔴 Interest rates can fluctuate.

🔴 Interest can be higher than other financing options, but it only accrues on what you haven’t repaid.

2. Invoice Factoring

Invoice factoring is a financial transaction in which you sell invoices to a third-party financial company, a factor, at a discount.

Usually, a factor will pay about 80-90% of the total invoice value. The factor collects payment directly from the customers on the invoices.

Once the customers pay in full, the factor pays you the remaining balance minus a fee for their services, a factoring fee.

Invoice Factoring: Key Pros and Drawbacks

🟢 Reduces credit risk and collection efforts

🟢 May be a good solution if unpaid invoices cause cash flow problems.

🟢 Debt-Free Funding.

🔴 You receive less than the total amount of the invoices.

🔴 Has a potential negative impact on customer relationships.

🔴 Can be complex to account for in bookkeeping.

3. Merchant Cash Advance (MCA)

With a merchant cash advance, you receive a lump sum of cash upfront for a percentage of your future credit card or debit card sales, plus a fee.

Instead of fixed monthly payments, the provider collects a percentage of the business's daily credit card sales, which is usually around 10-20% of daily sales,

In addition, the provider charges a fee that depends on the lender and your specific business.

On the other hand, since MCA isn’t a loan, your credit score and collateral aren’t determining factors for getting funding.

An important aspect is that MCAs are commercial transactions, so there is little government regulation.

As a result, it may end up quite hefty.

MCA: Key Pros and Drawbacks

🟢 Useful during slower sales periods.

🟢 No need to provide collateral.

🟢 Can be good if you have low credit scores.

🔴 More expensive compared to traditional loans.

🔴 Lack of government oversight can mean less protection for your business.

🔴 Not suitable unless you primarily process payments through credit cards.

4. Peer-to-Peer Lending

Peer-to-peer (P2P) lending is an alternative funding option that implies borrowing and lending money directly between individuals without the involvement of a traditional financial institution like a bank.

Borrowers and investors register on an online P2P lending platform, which connects them. You can see it as a big business match-making platform.

You apply for a loan on the P2P platform, specifying the loan amount, purpose, and other relevant details.

The platform assesses your creditworthiness, risk profile, and financial information to determine your eligibility for a loan.

Investors, often individuals looking to earn returns on their investments, review loan requests on the platform and choose which loans to fund based on factors like:

- Risk level,

- Interest rate,

- Loan term, and

- Your information.

One of the biggest appeals of P2P is that it has less vigorous procedures than banks.

Moreover, since these platforms operate at a lower cost, they can offer better conditions for all parties.

Nonetheless, the interest rates can be higher if your credit score is very low. It doesn’t come as a surprise since the lenders bear all the brunt in case something happens.

P2P: Key Pros and Drawbacks

🟢 Minimum requirements of credit history and security deposit.

🟢 Faster access to funds.

🟢 More flexibility in credit terms and interest rates.

🔴 For investors, it carries inherent risks, such as borrower default or late payments, which can impact ROI.

🔴 For borrowers, the rates can be high if you have a bad credit history and score.

How To Choose The Best Cash Flow Loan for Your Small Business?

Even within the same industry, no 2 small businesses are the same. Thus, a cash flow loan that works for one might have an adverse effect on another.

Simply put, you need to ensure that the loan not only meets your financial needs but also fits your business situation.

✨ Assess Your Cash Flow Needs — Determine why you need the cash flow loan and how much funding you require.

Evaluate your working capital requirements, expenses, and revenue projections to understand the amount you need.

✨ Evaluate Loan Options — Research different types of cash flow loans available to fully understand the terms, rates, and repayment structures of each option.

Go for a loan with favorable terms that align with your business cash flow and financial goals.

✨ Check Eligibility Requirements — Ensure that you meet the eligibility criteria set by lenders, such as credit score, revenue history, time in business, and other specific requirements.

✨ Review Repayment Flexibility—To avoid financial strain, choose a loan with manageable repayment terms that match your business's cash flow cycles.

✨ Understand Collateral Requirements — See if the loan requires collateral and evaluate the impact on your assets.

If you prefer an unsecured loan, search for lenders offering cash flow loans without collateral.

✨ Consider Lender Reputation — Research the reputation and credibility of potential lenders by reading reviews, checking customer feedback, and reviewing their track record.

You should select a lender with a solid reputation and good customer service.

✨ Read the Fine Print — Thoroughly review the loan agreement, including terms and conditions, fees, penalties, and repayment details.

Make sure you understand all aspects of the loan before signing any agreements.

How Can You Quickly Get a Cash Flow Loan with Puls Project?

Puls Project is a liquidity management and financing solution that caters to small businesses and provides solutions that deal with the essential aspects of cash flow management:

- Multibanking connectivity for a unified view of all financial transactions and operations.

- Loan possibilities to help you obtain and manage loans effectively.

- Cash flow planning to simplify financial management and ensure the accuracy of business decisions by using reliable data.

Regarding loans, once you connect your account, we calculate your company's credit limit based on your cash flow.

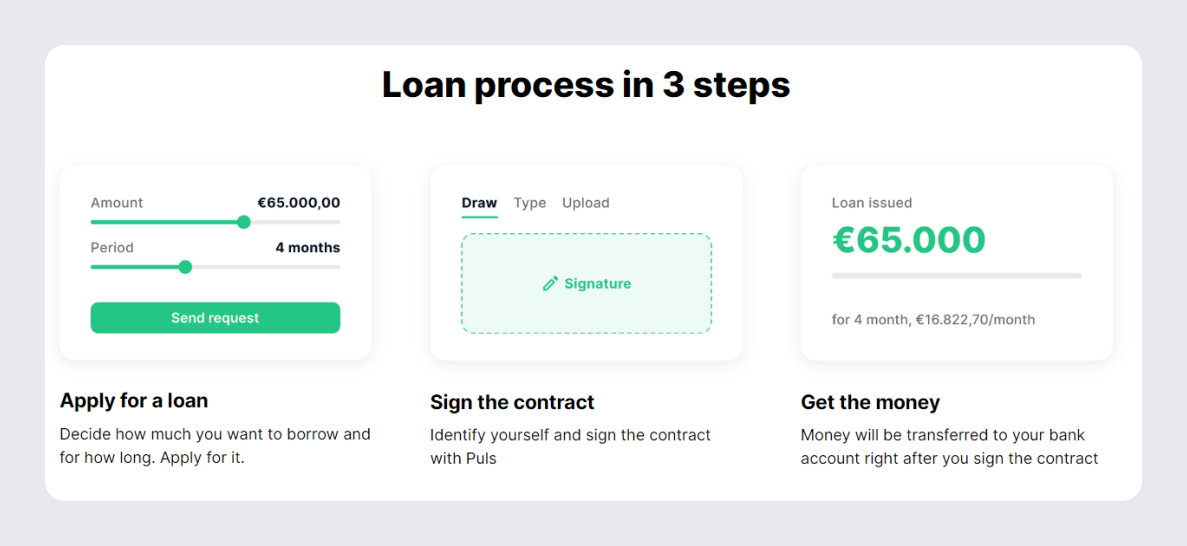

Step 1

Decide how much you want to borrow and for how long.

The process is transparent, and you’ll be able to suit the loan to your business needs and see the total cost, interest, and interest per month.

Step 2

We analyze your bank account transactions and, based on cash flow, determine how much credit your business can apply for.

The more data available, the better your score. Once we approve your credit, you can access the funds. The process usually takes up to 48 hours.

Step 3

Simply sign the contract and verify your identity by video. Pulse then transfers the funds to your business bank account the same day.

If Puls isn't a bank, why is getting a loan from us so simple?

🔥 It's because we issue loans from our credit fund registered with BaFin. Thus, there are no complex forms, banks, or other third parties involved.

Everything is straightforward.

🔥 Another great perk is that you can use only the amount you need, and the amount doesn’t impede your creditworthiness with banks.

🔥 Furthermore, thanks to our multi-banking connectivity and cash flow planner, you can see transactions, invoices, etc., from all your accounts in one place.

You can categorize and label transactions for even better management.

🔥 Transactions flow automatically to your dashboard and sync multiple times daily, providing a real-time view.

Each time, we also recalculate your credit availability.

And this is only the tip of the iceberg.

Want to see what lies underneath the surface?

Start with Puls Project for free to support your financial goals hassle-free.

Keep Learning

Open Banking: Unlocking Opportunities for Collaboration and Innovation in The Financial Industry

How Fintech is Disrupting The Traditional Lending Industry

FinTech vs. Banks – Competition or Collaboration? And What is Best for My Company?